Markets+ vs CAISO EDAM: Key Differences for Western Market Participants

Western power markets are entering a new era: two centralized day-ahead market paths are taking shape at the same time, SPP Markets+ and CAISO’s Extended Day-Ahead Market (EDAM).

For utilities, public power, marketers, and ISO/RTO participants with Western exposure, the decision is no longer abstract. EDAM begins activating in 2026, while Markets+ targets an October 2027 go-live for entities that met key registration deadlines. (caiso.com)

This post explains what’s different between the two constructs in ways that actually matter to practitioners: governance, footprint strategy, transmission and congestion treatment, charges and settlement implications, and seams risk.

It’s designed for Western market participants and for ISO/RTO operators and traders evaluating how a “two-market West” changes bidding, scheduling, hedging, and operations.

The Quick Definitions

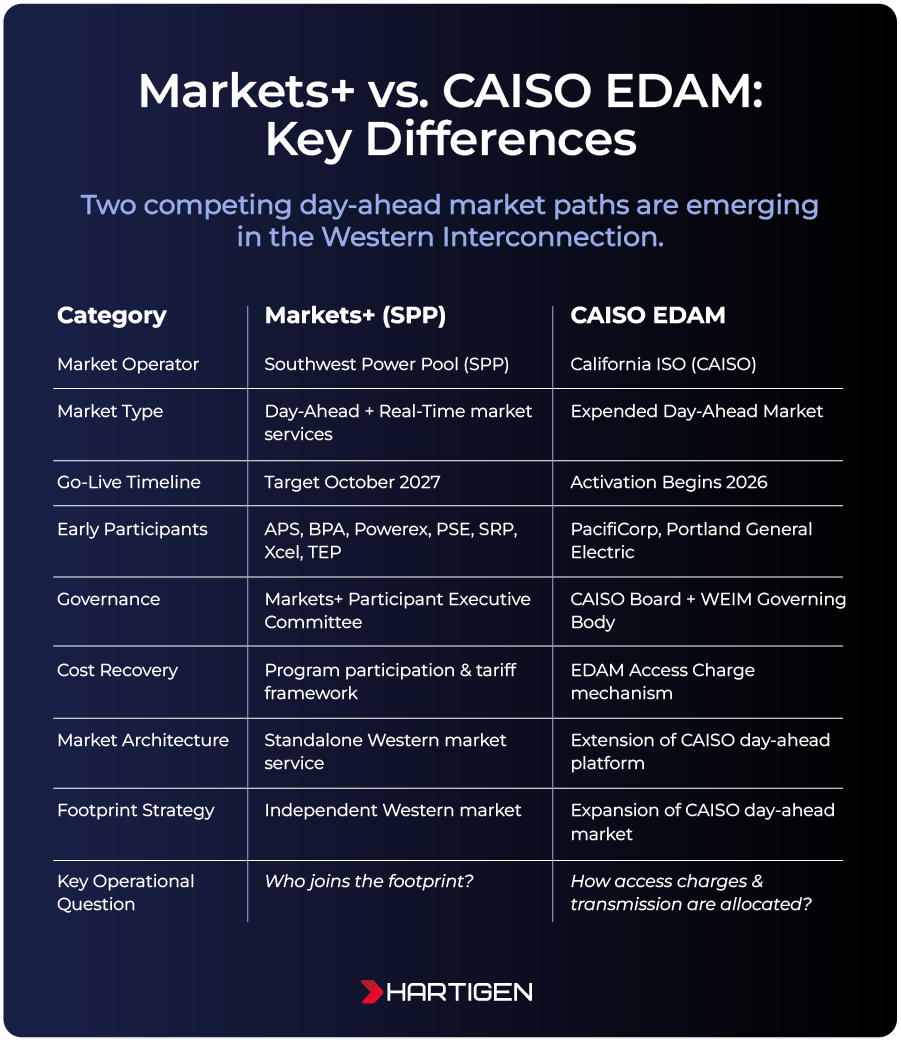

Markets+ (SPP): SPP describes Markets+ as a Western day-ahead and real-time market offering a “bundle of services” that centralizes day-ahead and real-time unit commitment and dispatch, aimed at improving reliability and expanding access to cost-effective energy in the West. (spp.org)

EDAM (CAISO): CAISO describes EDAM as a voluntary day-ahead electricity market that expands CAISO’s day-ahead optimization beyond its balancing authority area to participating external balancing areas, with the goal of improved efficiency and renewable integration through day-ahead unit commitment and scheduling across a larger area. (caiso.com)

Both are “day-ahead market” efforts. The hard part isn’t understanding the headline. It’s understanding how their implementation paths and market mechanics change costs and risk.

Key Differences Between Markets+ and CAISO EDAM

Where Each Market is on the Calendar

EDAM: activation starts in 2026

CAISO’s recent implementation update (March 2026) shows EDAM is deep into parallel operations with PacifiCorp as the first activation cohort (parallel operations began February 2026, with phased progress through March and April). (caiso.com)

CAISO’s public EDAM materials have long pointed to PacifiCorp (May 2026) and Portland General Electric (October 2026) activation timing. (westernenergymarkets.com)

Markets+: October 2027 target go-live (for entities meeting deadlines)

SPP’s Markets+ page states that indicating intent to participate by key registration deadlines is essential to ensure inclusion in the October 2027 go-live, with deadlines including BAs (Sept. 1, 2025), TSPs (Oct. 1, 2025), and Market Participants (Apr. 1, 2026).

FERC accepted Markets+ tariff provisions (subject to condition) in January 2025, moving Markets+ from “proposal” to an implementation program under FERC oversight. (spp.org)

Why this matters: If you’re making a “which market?” decision, the schedule alone changes your risk posture. EDAM has near-term operational reality (2026), while Markets+ has more runway (2027) but also clear gating deadlines for earliest inclusion.

KEY DIFFERENCE #1:

How You Join and What You are Joining

A subtle but practical distinction is the participation frame each market uses.

EDAM is an extension of CAISO’s day-ahead market

FERC’s Western markets explainer emphasizes that EDAM extends CAISO’s day-ahead market participation to entities outside CAISO’s balancing authority area, building on the model of CAISO’s real-time WEIM expansion. (ferc.gov)

That “extension” framing tends to pull participants into CAISO-aligned processes: business practice updates, market simulations, parallel ops, and settlement/tariff alignment workstreams designed around CAISO’s day-ahead platform. (caiso.com)

Markets+ is a standalone SPP Western market service offering

SPP positions Markets+ as a Western market offering (day-ahead plus real-time functions) that goes beyond imbalance-only services, with its own onboarding pathway and phase-two implementation structure.

The operational implication: In EDAM, you’re plugging into CAISO’s day-ahead architecture (plus DAME enhancements). In Markets+, you’re onboarding into SPP’s Western market service construct, with SPP as the market operator and a separate set of governance processes.

KEY DIFFERENCE #2:

Governance and Stakeholder Influence

Both markets have governance, but the “where decisions get made” differs in ways that matter for change management.

Markets+ phase-two governance structure

Public-power coverage notes Markets+ launched phase-two governance with a Markets+ Participant Executive Committee (MPEC) and associated working groups and task forces to guide implementation. (publicpower.org)

EDAM governance in the CAISO ecosystem

EDAM policy design was approved by FERC as part of CAISO’s DAME/EDAM filings, and CAISO’s Board and the WEIM Governing Body have been central to policy evolution and approvals for market expansion initiatives. (caiso.com)

What seasoned ISO/RTO participants know: governance location determines how fast rules evolve and how often operations teams must absorb changes. If you’re optimizing for “least change risk,” governance clarity is a major selection driver.

Day-ahead markets optimize generation commitment across large geographic areas.

KEY DIFFERENCE #3:

Cost Recovery Mechanisms and Market Charges (A Big One)

This is where differences get concrete and sometimes political, because they touch transmission revenue, congestion revenue allocation, and who pays for what.

EDAM: The Access Charge Framework (FERC-approved)

EDAM includes an “access charge” construct that FERC accepted via tariff revisions (initial access charge provisions were a focal issue in the earlier EDAM order, then revised and later accepted). (caiso.com)

CAISO’s settlements materials describe how the EDAM access charge is calculated and trued-up over time (including annual true-ups tied to projected vs actual collections for each EDAM transmission service provider). (caiso.com)

Separately, FERC has acted on EDAM’s congestion-related elements over time (including later refinements to congestion revenue allocation discussed in industry coverage), underscoring that EDAM’s cost and revenue allocation details have been an active implementation topic, not a footnote.

Markets+: Different Economic Questions Show Up First

Markets+ does not mirror EDAM’s access charge construct one-for-one. Instead, Markets+ discussions typically center on how the market offering (day-ahead + real-time) will deliver savings across a participating footprint and how participation and implementation costs are governed under the Markets+ program framework. FERC’s Markets+ order and SPP’s program materials define the tariffed structure and the implementation pathway.

Why this matters to participants: Charges shape your “all-in” economics. If you’re a transmission owner or closely tied to TSP revenue sufficiency, EDAM’s access charge mechanics can be a primary decision driver. If you’re a utility or marketer focused on portfolio value (commitment efficiency, congestion outcomes, imbalance reduction), Markets+ vs EDAM may be more about footprint + rules than any single fee line item.

KEY DIFFERENCE #4:

Transmission Treatment, Congestion, and the “Contract Path Reality” of the West

Both Markets+ and EDAM have to operate in a Western system that is historically more “contract path” oriented than many ISO/RTO footprints. That’s why many debates focus less on “Is there a DAM?” and more on “How will optimization behave against transmission rights and constraints?”

Translation for decision-makers: If you want the most robust “expected value” estimate, don’t start by arguing about one or two rule differences. Start by modeling:

Who will be in the market with you?

How well your system is interconnected with them?

What does your portfolio look like under day-ahead commitment and congestion outcomes?

KEY DIFFERENCE #5:

Seams Risk because the West May Operate as Two DAM Hubs

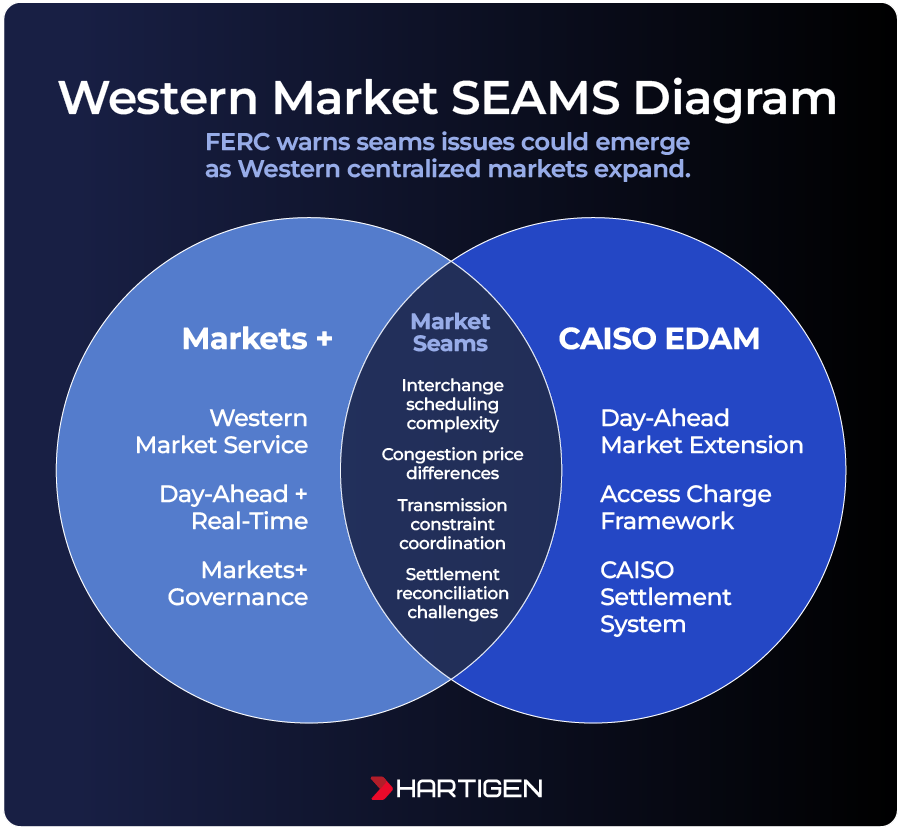

“If EDAM and Markets+ both expand, seams become unavoidable.”

FERC released a seams-focused white paper explicitly calling out that seams issues could arise as centralized markets expand in the West, and it notes the complexity and disconnected nature of the seam between Markets+ and EDAM in figures discussed in the paper.

What that means operationally:

Interchange scheduling and congestion assumptions can diverge across hubs

Financial exposure can concentrate at interfaces

Coordination processes (or lack of them) can create new sources of curtailment, uplift-like cost shifts, or settlement disputes.

This is familiar territory for ISO/RTO participants who already manage seams (PJM–MISO, SPP–MISO, NYISO–ISO-NE, etc.). The West is simply building its own version with the added complexity of a historically bilateral contracting culture.

FERC warns seams issues could emerge as Western centralized markets expand.

KEY DIFFERENCE #6:

Participant Momentum and Footprint Direction

Markets+ participants (Phase Two)

Markets+ publicly lists Phase Two participants (as of October 27, 2025) including entities such as Arizona Public Service, Bonneville Power Administration, Chelan County PUD, Grant County PUD, Powerex, Puget Sound Energy, Salt River Project, Tacoma Power, Tucson Electric Power, and Xcel/Public Service Company of Colorado.

EDAM early activators

CAISO’s EDAM materials and stakeholder communications have consistently identified PacifiCorp and Portland General Electric as the first implementation agreement signers and early activation cohorts.

The practical takeaway: if your counterparties and transmission neighbors are clustering into one construct, that clustering can outweigh theoretical pros/cons. Market choice often becomes a network effect problem.

A Practical Decision Framework: Which Market Fits Your Business?

Rather than treating this like a “which is better?” debate, most sophisticated participants evaluate Markets+ vs EDAM through three lenses:

1) Timeline and implementation risk tolerance

If you need day-ahead integration benefits sooner, EDAM’s 2026 activation timeline may be compelling. (caiso.com)

If you need more runway to build capabilities, Markets+’s 2027 target can align better especially if you’re coordinating across multiple internal teams (transmission, trading, settlements, IT, regulatory). (spp.org)

2) Transmission posture and settlement exposure

If your economics are highly sensitive to transmission revenue sufficiency and allocation mechanics, EDAM’s access charge and congestion revenue allocation evolution deserves deep attention. (caiso.com)

If your economics are driven more by broader day-ahead + real-time optimization value across a diverse footprint, Markets+ may be evaluated more on participation set, topology, and market rule stability under its phase-two governance. (publicpower.org)

3) Seams strategy (especially for ISO/RTO participants and large marketers)

If you’re active across West–RTO interfaces, plan for a two-DAM West and treat seams as a core workstream, not a postscript. FERC has explicitly focused on seams issues arising from Western centralized market expansion.

Readiness Work is the Real Cost

Both markets require serious, multi-year readiness. CAISO’s onboarding materials show EDAM implementation includes structured onboarding tracks (integration testing, simulation, parallel ops, training, and settlements readiness). (caiso.com)

SPP’s Markets+ page similarly emphasizes onboarding via formal processes and highlights registration deadlines tied to go-live inclusion.

Participants that do best tend to invest early in:

A single operating model for market decisions (who decides what, when)

Disciplined assumptions and approvals (forecasts, outages, constraints)

Robust settlement validation and dispute workflows

Seams-aware scheduling and congestion strategy

Where Hartigen Fits

Decision Infrastructure for Markets+ (and every market change after)

Western day-ahead market expansion isn’t a one-time project. It’s a permanent operating environment: ongoing tariff changes, evolving business practices, shifting participant footprints, and growing seams complexity.

“Hartigen is built to be decision infrastructure for this reality helping teams convert market change into controlled, auditable execution instead of scattered spreadsheets and reactive firefighting.”

For Markets+ participants and prospective participants, Hartigen supports:

Market change management that survives the next revision.

Markets+ is already in phase-two governance and implementation, with defined onboarding gates and a 2027 go-live target for early cohorts. (publicpower.org)

Hartigen helps you track requirements, decisions, owners, and evidence in one place so deadlines and readiness aren’t disconnected.

Cross-functional alignment on the daily “what do we believe?” decisions.

Day-ahead markets reward organizations that can align forecasting, operations, and commercial positions quickly and consistently. Hartigen turns those assumptions into a shared system of record so trading, operations, settlements, and regulatory teams operate from the same source of truth.

Preparation for EDAM/DAME realities even if your path is Markets+.

Many organizations must remain EDAM-aware because counterparties, neighbors, or seams exposures will be EDAM-linked. Hartigen publishes practical guidance on CAISO EDAM/DAME initiatives and supports organizations preparing for CAISO’s more integrated Western market environment.

Seams readiness as a first-class workflow.

FERC’s seams work highlights the complexity of interfaces that could develop between Markets+ and EDAM.

Hartigen helps you operationalize seams strategy: schedule assumptions, constraint tracking, settlement reconciliation, and “what changed” governance so seams don’t become the place where value leaks.

In short: Markets+ vs EDAM is a strategic choice, but market change capability is the enduring advantage. Hartigen helps you build that capability once and reuse it for every market transition that follows.

The Bottom Line

Markets+ and CAISO EDAM share the same macro goal: expand the benefits of centralized optimization into the Western day-ahead timeframe. The meaningful differences are in implementation timing, governance pathways, charge and allocation mechanisms, transmission/congestion handling, and seams risk. (caiso.com)

EDAM is entering operational reality in 2026 with early activations like PacifiCorp and PGE.

Markets+ is moving through implementation with a published October 2027 target go-live for entities that met key registration deadlines and with phase-two participants publicly listed.

If you want to win in either world, EDAM, Markets+, or a two-market West, the biggest differentiator won’t be a single tariff clause. It will be how well your organization can turn market complexity into repeatable, high-confidence decisions.

Hartigen is built to do exactly that.